Ever submitted a loan application feeling confident, only to have it rejected or approved for a smaller amount than you expected?

You’re not alone.

Many hardworking Malaysians face this frustrating situation. The reason often boils down to a single, powerful number that banks scrutinize closely: your Debt Service Ratio (DSR).

Think of your DSR as your financial report card for lenders. It’s a simple percentage that tells them, “Can this person comfortably handle more debt?”

As a financial planner, I don’t just help people invest; I help them build a solid foundation. And understanding your DSR is the cornerstone of that foundation. Let’s pull back the curtain and calculate your DSR exactly like a banker would.

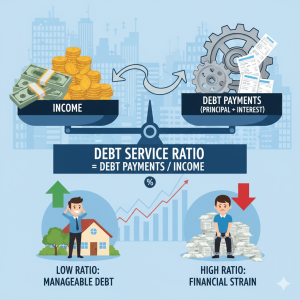

What Exactly is the Debt Service Ratio (DSR)?

In simple terms, your DSR is the portion of your monthly income that goes towards repaying your debts.

Banks in Malaysia use this ratio to assess your credit risk. A low DSR means you have a healthy cash flow and are likely a reliable borrower. A high DSR is a red flag, indicating you might be overstretched and could struggle with new repayments.

The Banker’s Formula: How to Calculate Your DSR

Ready for the simple math? Here is the standard formula used by most financial institutions in Malaysia:

DSR = (Total Monthly Commitments / Total Monthly Income) x 100

Let’s break this down with a real-life Malaysian example.

Step 1: Calculate Your Total Monthly Commitments

This is the total of ALL your monthly debt obligations. Be honest and include everything:

- Housing Loan: RM1,500

- Car Loan: RM800

- Personal Loan: RM400

- Credit Card Payments: (This is key!) As a standard practice, banks will calculate your credit card commitment for DSR purposes as a percentage of your total outstanding balance, not the minimum payment shown on your statement. They typically use 5% of your outstanding credit card balance.

- If you have a total credit card balance of RM10,000, your commitment is RM500 (5% of RM10,000).

- PTPTN Loan: RM200

- Any other ongoing loans.

Total Monthly Commitments for our example:

RM1,500 + RM800 + RM400 + RM500 + RM200 = RM3,400

Step 2: Determine Your Total Monthly Income

This includes your fixed monthly salary and any guaranteed side income. If you have variable income (like commissions or freelance work), banks will often take an average.

- Net Salary: RM6,500

- Fixed Rental Income: RM500

Total Monthly Income for our example: RM7,000

Step 3: Plug It Into the Formula

Now, let’s do the calculation:

DSR = (RM3,400 / RM7,000) x 100

DSR = 0.4857 x 100

DSR = 48.57%

The Golden Number: What’s a “Good” DSR in Malaysia?

So, is 48.57% good or bad?

While different banks have different thresholds (and it can vary based on your income level and the type of loan), here’s a general rule of thumb:

- Below 30%: Excellent! You have great financial flexibility.

- 30% – 60%: Manageable, but this is the zone where banks become cautious. For new applications, most banks prefer a DSR below 60% after including the new loan’s repayment. Some even have a stricter limit of 50-55%.

- Above 60%: Danger zone. Your loan application will likely be rejected as you are considered over-leveraged.

In our example, a DSR of 48.57% is generally acceptable, but there might not be much room left for a large new loan.

Why Should You, as a Malaysian, Care About Your DSR?

- Smoother Loan Approvals: This is the most immediate benefit. Knowing your DSR before you apply saves you time, disappointment, and prevents multiple rejections from hurting your CCRIS record.

- Financial Stress Test: Your DSR is a quick health check. A high number is a clear warning sign that you’re living paycheck-to-paycheck and are vulnerable to any financial emergency.

- Empowerment for Big Life Goals: Whether it’s buying your first home, upgrading your car, or getting a loan for a business, mastering your DSR puts you in the driver’s seat.

3 Actionable Steps to Improve Your DSR Today

If your DSR is higher than you’d like, don’t panic. Here’s what you can do:

- Increase Your Income: This is the most straightforward way. Consider a side hustle, ask for a raise, or look for a higher-paying job.

- Reduce Your Debt: Focus on paying down high-interest debt first, like credit cards and personal loans. Even a small reduction in your credit card balance can significantly lower the “5%” commitment calculation.

- Avoid New Debt: Put a temporary hold on taking any new loans. Consolidate existing debts if it leads to a lower overall monthly commitment.

Let’s Have an Honest Conversation About Your Number

Calculating your DSR is a powerful first step. But what comes next? How do you create a plan to lower it? What if you have dreams but your DSR is holding you back?

This is where a structured financial plan makes all the difference.

I offer a complimentary, 15-minute DSR & Strategy Call. This is not a full financial plan. It’s a quick, focused session where we will:

- Verify your DSR calculation.

- Identify the #1 debt that’s hurting your score the most.

- Outline the clear, logical next steps you can take to improve your financial position.

This call is for anyone who is serious about getting their finances loan-ready and wants a clear, expert perspective on how to do it.

You don’t have to navigate this alone. Just leave your details by clicking the button below. I will reach out to you and see if we would be a good fit for each other.

Let’s have a conversation, not a commitment.

Or, join my email list by clicking here if you are not ready to connect yet.

Disclaimer: This post is for informational purpose only. You should use judgment and conduct due diligence before taking any action or implementing any plan suggested or recommended in this article. Specific DSR thresholds and calculations may vary between financial institutions in Malaysia.